Real Estate

Buying Properties with Sitting Tenants: What Every Investor Must Know

Buying properties with sitting tenants is often misunderstood in the UK property market, yet it offers unique investment advantages. While some investors hesitate due to tenancy rights and vacant possession concerns, experienced landlords recognise immediate rental income benefits.EAGuaranteedRent supports landlords and investors by simplifying due diligence, ensuring compliance, and providing ongoing management assistance for tenanted property investments.

What Does Buying Properties with Sitting Tenants Actually Mean?

A sitting tenant is a person who legally occupies a property under an existing tenancy agreement at the time of sale. When a landlord sells a property, the tenant remains, and the buyer simply becomes the new landlord.

This is more common than most people realise. Portfolio landlords selling up, estate sales, and even institutional investors all list tenanted properties regularly. The key point is: the tenancy does not end on completion day. It transfers.

| Vacant Property | Tenanted Property | Key Difference |

| No rental income immediately | Rental income from day one | Cash flow |

| Full market value purchase | Typically 10 to 25% below market | Purchase price |

| Free to refurbish straight away | Must respect tenancy terms | Flexibility |

| Find a tenant yourself | Tenant already in place | Occupancy risk |

Types of Tenancies You May Inherit

Not all sitting tenants have the same legal protections. The type of tenancy determines your rights as the incoming landlord and the process required if you ever want to regain possession.

Assured Shorthold Tenancy (AST)

The most common type in England and Wales. An AST transfers automatically to the buyer. If the fixed term has ended, and the tenancy is running on a rolling basis. You can serve a valid Section 21 notice to regain possession, subject to legal requirements being met.

Regulated Tenancies (Pre-1989)

These are rarer but far more complex. Regulated tenancies grant the tenant the right to live in the property for life in many cases, with rent controlled by a Rent Officer. Buying a property with a regulated sitting tenant often means a significant discount, sometimes 30 to 40 per cent below market value. However, it also comes with stricter limitations on how you can use or manage the property.

Company Lets and Non-Statutory Arrangements

Some properties are let under company tenancy agreements or informal arrangements. These fall outside standard residential tenancy law and require separate legal review. Always obtain full copies of all tenancy documentation before exchanging contracts. Working with an experienced agent when entering this market can save significant time and money.

The Discount Factor: Why Sitting Tenants Reduce Purchase Price

One of the main attractions of buying tenanted properties is the built-in discount. Markets price these below vacant equivalents for three reasons:

- Restricted buyer pool: Owner-occupiers cannot move in, so only investors bid, reducing competition.

- Perceived management risk: Some buyers factor in the uncertainty of dealing with an existing tenant.

- Below-market rent: If the existing rent is lower than current market rates, the yield calculation makes the price less attractive at full value.

As a result, a property worth £250,000 when vacant may sell for £200,000 to £220,000 with a sitting tenant on a standard AST. With a regulated tenancy, the price can drop even further due to stricter tenant rights and reduced flexibility. This discount is not a sign of a bad deal; it is an investment opportunity.

Legal Obligations When You Become the New Landlord

Taking on a sitting tenant means taking on a set of legal responsibilities from completion day. This is not an area to cut costs. Once you own the property, professional property management services can handle compliance checks, rent collection, and maintenance coordination efficiently. Ignorance of these obligations is not a legal defence. Below is a structured overview of the key duties:

| Obligation | What It Means | Timing |

| Notify the tenant in writing | Inform the tenant of the new landlord’s details and payment instructions | Within 2 months of completion |

| Register the deposit | Ensure the deposit is protected in a government-approved scheme | Within 30 days if not already done |

| Provide EPC, Gas Safety Certificate, EICR | Confirm valid certificates are in place | Before or at tenancy transfer |

| Maintain the property | Keep the property in a safe, habitable condition | Ongoing duty |

| Serve correct notices | Use correct legal forms if you ever wish to end the tenancy | As required — follow statutory process |

It is strongly advisable to instruct a solicitor experienced in landlord and tenant law to review all documents before you complete on the purchase. This reduces the workload for investors, especially those managing multiple tenanted properties within a growing property portfolio.

Carrying Out Due Diligence Before You Buy

Due diligence on a tenanted property goes further than on a vacant one. You are not just assessing bricks and mortar, you are assessing a tenancy relationship. Here is what to investigate:

- Request the full tenancy agreement and all addenda.

- Obtain a full rental payment history check for arrears, late payments, or disputes.

- Confirm the deposit amount and the scheme it is registered with.

- Review all certificates: Gas Safety Record, EPC, and EICR.

- Check whether a How to Rent guide was served to the tenant.

- Speak to the selling landlord about the tenant’s history and relationship with the property.

Any gap in compliance on the seller’s side becomes your problem after completion. If the original Section 21 notice cannot be served because a How to Rent guide was never issued, you inherit that restriction. Negotiate for price reductions or seller rectification where deficiencies are found.

The Underrated Advantage: Long-Term Tenants Are Often Your Best Tenants

This is something rarely highlighted in mainstream investment guides: tenants who have lived in a property for years are often very stable and reliable. They tend to stay long-term, providing consistent rental income and peace of mind for investors. They have already demonstrated long-term commitment to the property. Void periods and re-letting costs are among the highest hidden costs in buy-to-let a long-standing tenant eliminates both.

This is the point many first-time investors miss. The market prices the property lower due to perceived risk. If the tenant pays regularly, maintains the property, and plans to stay long-term, the investment becomes very secure. In this case, you have effectively acquired a low-risk income asset at a discounted price. The tenant is not a problem; they are a core part of the investment case.

When Buying Properties with Sitting Tenants May Not Be Right for You

This strategy suits experienced investors and portfolio builders, but it is not the right fit for every buyer. You should be cautious if:

- You intend to live in the property yourself and need it vacant on completion.

- You want to carry out significant refurbishment work immediately after purchase.

- The property has a regulated tenancy with complex rights and limited rental upside.

- Due diligence reveals rent arrears, compliance failures, or disputed occupancy.

- You are not prepared to manage an existing tenancy relationship from day one.

Frequently Asked Questions

Can I evict a sitting tenant after buying the property?

Yes, but only through legal processes. For AST tenants on a periodic tenancy, you can serve a Section 21 notice if all compliance requirements are met. You cannot simply ask a tenant to leave because you have bought the property. Attempting to do so without following the correct procedure may constitute illegal eviction.

Do I need to re-sign a new tenancy agreement with the sitting tenant?

No. The existing tenancy agreement transfers automatically to you on completion. You become the landlord under the same terms. You can choose to enter into a new agreement at a future date if both parties agree, but this is not legally required.

What happens to the tenant’s deposit when I buy the property?

The deposit should transfer to you on completion, or the seller may return it to the tenant with a new deposit taken. You must protect the tenant’s deposit in a government-approved scheme within 30 days of receiving it. The tenant must also be given the prescribed information about that scheme.

Can I increase the rent after buying a tenanted property?

For AST tenancies, you can increase the rent but only through the correct process. During a fixed term, you are bound by the rent stated in the agreement unless a rent review clause is included. For a periodic tenancy, serve a Section 13 notice giving at least one month’s notice, or longer if stated.

Will mortgage lenders fund a property with sitting tenants?

Most buy-to-let mortgage lenders will lend on properties with sitting tenants on standard ASTs. However, some lenders restrict lending on properties with regulated tenancies or non-standard occupancy arrangements. Always inform your mortgage broker of the tenancy status before applying, and confirm the lender’s specific criteria.

Is buying a tenanted property a good investment strategy?

When approached correctly, yes. Immediate rental income, a discounted purchase price, and no initial void periods make this highly capital-efficient property investment. The key is thorough due diligence, legal compliance from day one, and understanding the exact type of tenancy you are inheriting.

Conclusion

Buying properties with sitting tenants can be a highly rewarding strategy for informed investors. The purchase discount, immediate rental income, and tenancy stability create significant advantages. Success depends on understanding the legal framework, landlord obligations, and tenancy specifics. With careful due diligence and professional guidance, a tenanted property becomes a strategic, long-term investment advantage.

Walk along any beach in Punta Cana, Las Terrenas, or Puerto Plata today, and you’ll notice something that wasn’t there ten years ago: cranes.

Tourism in the Dominican Republic stopped being just a hospitality story a while back. It became a real estate story. Every record-breaking year of visitor arrivals has translated, almost directly, into property demand in the coastal areas of the Dominican Republic.

What used to be a market built around hotel rooms is now a market built around homes, condos, and second residences owned by both Dominicans and foreigners who fell in love with the coast on vacation and decided to stay. That shift is the reason coastal land values keep climbing, and it’s the reason this guide exists.

Why Tourism Creates Long-Term Property Demand in Coastal Areas of the Dominican Republic

The Dominican Republic closed 2025 with 11.6 million visitors, the best year in the country’s tourism history. That number isn’t just a tourism statistic. It’s the starting point of a chain reaction that ends with someone buying a condo two kilometers from the beach.

Here’s how it actually plays out, and why it isn’t a coincidence.

- A visitor lands in Punta Cana or Las Terrenas for a week, falls for the water, the warmth, the pace of life, and starts thinking about a second home before their flight even leaves.

- Vacation rentals turn that interest into income proof. Once a buyer sees that a beachfront apartment can be rented out to other tourists for a healthy chunk of the year, the property stops being a lifestyle purchase and becomes an investment with numbers behind it.

- Rental income attracts more serious capital, and serious capital pushes for better roads, better airports, better connectivity.

- Once an area is easy to reach and easy to live in, international buyers from the US, Canada, and Europe move from “maybe someday” to “let’s look at listings.” Fifth, residential communities form around that buyer base, gated developments, beach clubs, and walkable coastal towns built specifically for people who want resort living year-round rather than for a week.

This is exactly why property demand in the coastal areas of the Dominican Republic keeps compounding instead of leveling off. Tourism isn’t a side input here. It’s the engine.

Coastal Destinations Where Property Demand Is Growing the Fastest

Not every coastal town is growing at the same speed, and knowing the difference matters more than people think.

Punta Cana

Punta Cana remains the country’s flagship market, and for good reason. It has the densest concentration of international flights, the most established short-term rental economy, and the deepest pool of buyers comparing properties before committing. Property demand here is driven by proven returns, not speculation.

Las Terrenas

Las Terrenas has built its reputation on a more boutique, European-influenced lifestyle, attracting buyers who want charm over scale. French, Italian, and German investors have driven much of the early growth here, and that international mix keeps pushing property demand upward, especially for smaller villas and beachfront condos.

Cabarete

Cabarete built its identity on wind, waves, and an adventure-sport crowd that never really left. Surfers and kiteboarders who visited once often come back to buy. That loyalty creates a steady, less speculative kind of property demand tied to lifestyle rather than resale flipping.

Puerto Plata

Puerto Plata combines cruise port traffic with a more affordable entry point than Punta Cana, which makes it attractive to first-time coastal investors. Renewed infrastructure investment and Atlantic coastline views are pulling new buyer attention toward this once-overlooked northern hub.

Samaná

Samaná still feels undiscovered, which is exactly its appeal. Whale-watching season, dramatic peninsula views, and limited existing development mean buyers here are betting on the next wave of growth. Investors who got into Las Terrenas early are now eyeing Samaná the same way.

How to Find the Right Investment Opportunities with Dominican Republic Property Listings

Once you understand where property demand in the coastal areas of the Dominican Republic is heading, the next challenge is separating genuine opportunity from an overpriced listing with a nice photo.

Comparing listings properly means looking past the beachfront photo and into the numbers underneath it. Price per square meter in the same micro-zone, not just the same town, tells you more than any brochure. A unit two streets back from the water in Las Terrenas can be a smarter buy than a flashier one directly on the sand, depending on what you’re trying to achieve with the property.

Location matters, but so does intent. A buyer chasing rental yield needs proximity to the beach, walkability to restaurants, and a management company already operating nearby. A buyer planning a personal retirement home can prioritize quiet over rental traffic.

This is where working through trusted, well-organized Dominican Republic property listings actually pays off. A platform that lets you filter by region, price history, and property type saves weeks of back-and-forth with agents who may only show you their own inventory. The buyers who do best here treat listings the way they’d treat a stock screener: comparing across the board before falling in love with any single option.

What Buyers Should Consider Before Investing in Coastal Property

Beyond location and listings, a few practical checks decide whether your investment performs.

Legal Due Diligence

Always confirm zoning, ownership history, and any liens before signing anything. A lawyer independent from the seller protects you from surprises that surface only after the deal closes.

Property Titles

Dominican title law (Título de Registro) differs from US or European systems. Confirm the title is registered, clean, and free of disputes before transferring a single peso.

Rental Potential

Check actual occupancy data from nearby properties, not projected estimates from a developer’s brochure. Real numbers from real seasons tell the truth about return potential.

Infrastructure & Accessibility

Distance to the airport, road quality, and water and power reliability affect both your lifestyle and your resale value. A stunning villa down a flooded dirt road loses appeal fast.

Long-Term Appreciation

Look at five-year price trends in the specific zone, not the whole region. Some pockets appreciate steadily while neighboring ones stagnate, even within the same coastal town.

How You Can Sell Your Properties to Reach More Buyers and Investors

Buyer interest in Dominican coastal property isn’t slowing down, and that creates opportunity for sellers too, but only if your property is visible to the right audience.

International buyers researching from the US, Canada, or Europe rarely walk into a local office. They search online first, compare options, and shortlist properties weeks before ever landing in the country. If your listing isn’t where they’re looking, you’re invisible to a huge share of qualified demand.

Easy listing management matters just as much as exposure. Sellers juggling multiple inquiries via WhatsApp, email, and word of mouth lose serious buyers to slower-moving competitors with organized platforms. What actually closes deals is connecting with prospects who are already qualified, already comparing coastal markets, and already motivated by the same tourism-driven demand fueling this entire conversation.

This is exactly the gap a platform like Roof360 is built to close. If you’re a property owner or developer trying to reach serious buyers without losing weeks to scattered inquiries, you can register your property on Roof360 and put your listing in front of the audience actively searching for coastal opportunities in the Dominican Republic right now.

Conclusion: Tourism Is Creating Lasting Opportunities in Coastal Real Estate

Tourism in the Dominican Republic isn’t a passing wave; it’s a sustained current reshaping the coastline year after year. Every new arrival record adds fuel to property demand in the coastal areas of the Dominican Republic, and that demand isn’t slowing as new destinations like Samaná and Puerto Plata emerge alongside established leaders like Punta Cana.

For investors and homeowners alike, this means continued appreciation for those who buy thoughtfully and sell strategically. Whether you’re searching trusted listings to find your next investment or preparing to register your property on Roof360 to reach serious buyers, the opportunity in Dominican coastal real estate has never been more real.

Owning a piece of architectural history is a deeply rewarding stewardship. Whether it is a grand Victorian with intricate gingerbread trim, a stately Georgian featuring hand-carved millwork, or a mid-century modern jewel defined by clean geometric lines, historic properties possess an undeniable character and soul. These structures stand as tangible links to our collective past, showcasing craftsmanship, material quality, and design philosophies that are virtually impossible to replicate in modern tract housing.

However, the passage of time introduces a relentless physical challenge to the preservation of these aging structures. Over decades, structural settling, fluctuating environmental humidity, UV radiation, and biological elements work continuously to degrade the building envelope. Preserving the authentic charm of a historic property without stripping away its historical integrity requires moving past quick, contemporary renovation patches. It demands a highly disciplined approach centered on material authenticity, structural reversibility, and proactive environmental defense.

1. Embracing the Principle of Minimal Intervention

The foundational rule of historical preservation—codified by conservation institutions worldwide—is to repair rather than replace. When an owner encounters a weathered architectural element, such as a water-damaged window sill or a cracked plaster crown molding, the immediate contemporary impulse is often to tear it out and install a modern, synthetic alternative.

This reactive approach systematically destroys the historic fabric and financial equity of the property. True preservationists practice minimal intervention. If a section of a historic heart-pine floor or exterior clapboard is damaged, the correct path is to perform a localized repair. For example, wood rot can be methodically excavated and stabilized using specialized structural epoxies, preserving the surrounding original timber. By keeping as much of the original material matrix intact as possible, you protect the authentic texturing, slight imperfections, and historical weight that define period architecture.

2. Prioritizing Material Authenticity and Traditional Craftsmanship

When material replacement becomes structurally unavoidable due to severe rot or mechanical failure, sourcing authentic, period-accurate materials is non-negotiable. Modern construction materials—such as vinyl siding, engineered MDF trim, and Portland-cement-based mortars—are chemically and structurally incompatible with old buildings.

Consider the soft, lime-based mortars utilized in historic brick masonry. If a modern contractor uses hard, rigid Portland cement to repoint a historic soft-brick wall, the new mortar will resist natural thermal expansion. When the temperature shifts, the unyielding cement will crush the surrounding historic bricks, causing severe face-spalling and structural degradation. Preservation requires tracking down specialized trade professionals who understand traditional techniques, such as mixing appropriate lime-putty mortars or sourcing old-growth lumber. Utilizing materials that match the original composition ensures the home breathes and flexes exactly as its architects intended.

3. Developing an Invasive Defense System Against Biological Subversion

The primary threats to an aging building do not always manifest as macro-structural failures or roof leaks. Frequently, the most destructive forces are microscopic or highly secretive biological invaders that exploit the natural nooks, deep wall voids, and porous structural timbers characteristic of old construction.

Because historic homes lack modern vapor barriers, sealed crawlspaces, and pressure-treated framing, they are highly vulnerable to wood-boring beetles, subterranean termites, and opportunistic rodents. If a biological infestation is left unmanaged within an old structural frame, it can quietly consume load-bearing beams from the inside out, leading to irreversible structural failure before surface signs ever appear. Protecting these vulnerable materials requires a continuous, highly specialized defensive strategy that respects the historic architecture.

In regions known for intense seasonal shifts and aggressive pest pressures, generic, over-the-counter pest solutions fail completely because they do not account for the complex layout of period walls. Securing a highly disciplined, regional pest control company in Dallas ensures that historical properties undergo rigorous, low-impact monitoring and structural exclusion. Professional conservation-minded crews deploy targeted, non-repellent baiting arrays and specialized borate treatments directly into original framing timbers rather than saturating historical spaces with harsh, destructive chemical washes. This precise, integrated approach eliminates hidden biological activity without altering the visual patina or chemical stability of the original wood, insulating the home’s foundational heritage from decay.

Abra Kadabra Environmental Services

4. The Philosophy of Reversible Upgrades

A historic home must function as a liveable, comfortable modern sanctuary if it is to survive into the next century. This means that electrical grids, climate control mechanics, and plumbing lines must inevitably be brought up to modern regulatory safety standards.

The secret to executing these vital infrastructure transitions safely is adhering to the rule of reversibility. Any modernization project performed on a historic property should be executed in a manner that allows it to be completely removed in the future without causing permanent damage to the primary historic structure. For instance, rather than cutting massive, destructive ductwork channels through original plaster ceilings to install a traditional central HVAC system, a preservationist will opt for a low-profile, ductless mini-split network or route small-duct high-velocity lines through existing utility chases and closets. This structural foresight preserves pristine interior surfaces while delivering modern environmental efficiency.

Conclusion

Preserving the authentic charm of a historic property is a meticulous, lifelong labor of respect, patience, and deliberate engineering. It is an intentional victory achieved by choosing localized material repairs over superficial replacements, enforcing strict historical material authenticity, implementing targeted biological defense systems, and ensuring all modern utility upfittings remain entirely reversible. By accepting the role of a dedicated steward rather than a disruptive renovator, you actively protect your home from structural decay and cultural dilution. Ensuring that these protective preservation safeguards are woven into your property’s ongoing maintenance rhythm guarantees that its unique character, expert craftsmanship, and historical soul will endure to inspire, comfort, and captivate generations to come.

Real Estate

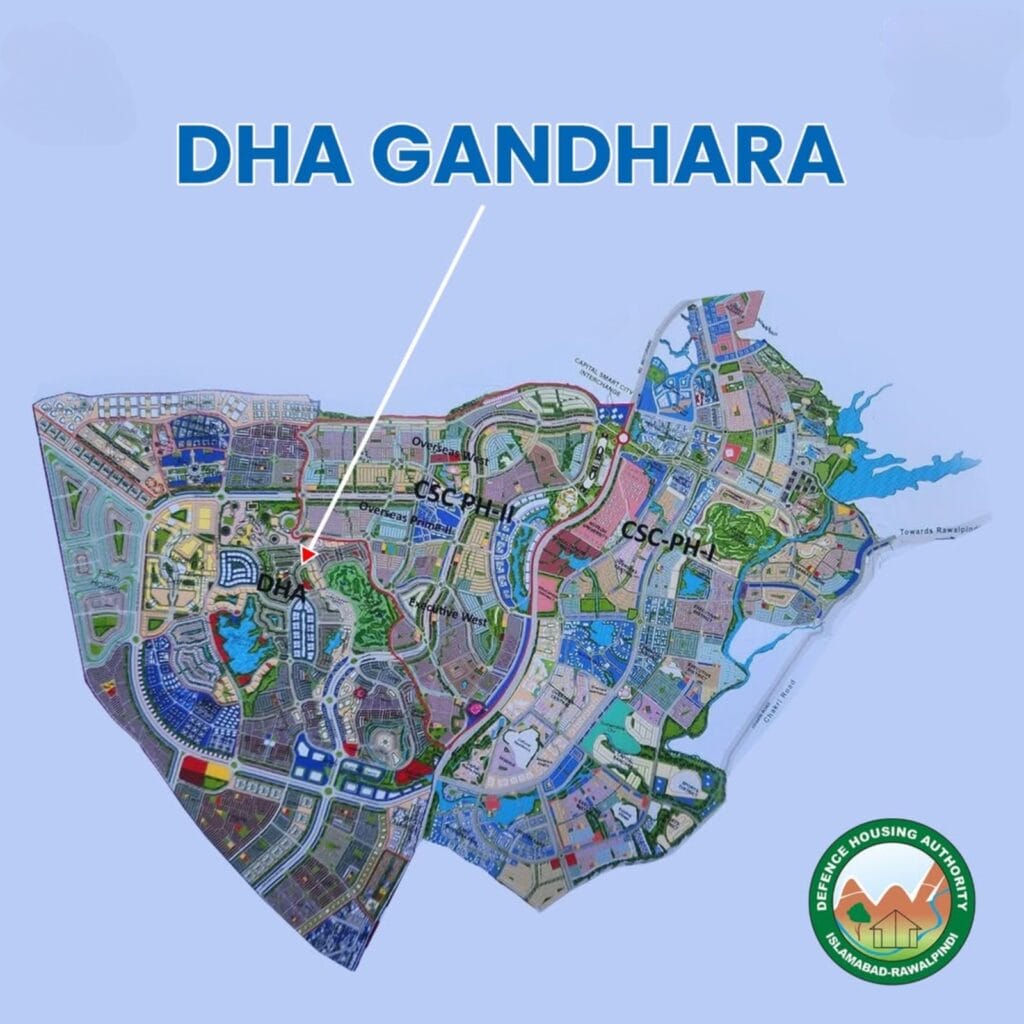

DHA Gandhara Islamabad Location Analysis – A Complete Guide to Accessibility and Connectivity

DHA Gandhara Islamabad is rapidly making waves in the real estate sector of the twin cities. While people track the file rates and updates to the launches, one thing is most important to keep in mind: location. One of the most important factors is the accessibility, neighbouring properties and development of infrastructure for any housing scheme. In all these fields, it seems like DHA Gandhara Islamabad is well ahead.

It is situated in the fast growing airport corridor, and will be likely to have access to major roadways as well as residential areas. The strategic location of DHA Gandhara Phase 9 Islamabad has attracted many investors interested in the appreciation of the property and the future residential opportunities.

This article delves into the DHA Islamabad location, its proximity, key landmarks, and travel options, as well as the potential effect these connections could have on the value of the property.

DHA Gandhara Islamabad – A Brief Overview

DHA Gandhara Islamabad, also known as DHA Gandhara Phase 9 Islamabad, is the new lifestyle land developing project that will define the modern lifestyle in the vicinity of Islamabad.

The project is being built under the safe brand DHA and it is expected to provide a residential district, a commercial district, an educational district and a recreational district.

The project’s blend of contemporary planning and strategic location has garnered investor interest.

Its location within the airport growth corridor makes it one of the most promising developments in the region in the future.

- Upcoming DHA mega project

- Planned mixed-use development

- Strong investor interest

- Modern infrastructure vision

- High future growth potential

DHA Gandhara Islamabad Location – The Biggest Advantage

The project’s best investment aspect is the DHA Gandhara Islamabad location. The project is projected to be located in close proximity to Islamabad International Airport, which is one of the key transportation hubs in the area.

It is also situated near to Motorway M-2 and Chakri Interchange, which facilitates easy connectivity with Islamabad, Rawalpindi, Lahore and other major cities. This is what is expected from the sort of connectivity that will contribute greatly to the property’s value upgrading in the future.

- Near Islamabad International Airport

- Access to Motorway M-2

- Close to Chakri Interchange

- Strategic airport corridor placement

- Strong appreciation potential

Connectivity to Islamabad International Airport

The key factor for investors to choose DHA Gandhara is the ease of access to Islamabad International Airport. In modern housing projects, situated in proximity to international airports, stronger market demand for commercial and residential properties can be observed.

Airport connectivity is useful for the business community, for those who are coming back from overseas Pakistan and for frequent travellers. The surge of development around airports often brings more investor interest and value in the local residential area.

- Quick airport access

- Increased investor demand

- Better commercial prospects

- Ideal for overseas buyers

- Long-term value enhancement

Access to Motorway M-2

Motorway M-2 is the one of the most significant transportation corridors of Pakistan which links Islamabad and Lahore to the other major cities of Punjab. The Motorway will have a major impact on DHA Gandhara Islamabad.

The motorway connection makes it easy to travel from residents and businesses, reducing travel time and enhancing connectivity. This can lead to long-run property value growth and other infrastructure benefits.

- Direct regional connectivity

- Reduced travel times

- Better commercial access

- Improved mobility

- Strong future demand

Rawalpindi Ring Road Connectivity

The Rawalpindi Ring Road project is anticipated to be one of the most impactful infrastructural development initiatives in the area. The road network is intended to enhance traffic flow, link up key residential and commercial areas.

This is likely to have a positive impact on DHA Gandhara Phase 9 Islamabad. Greater accessibility will usually lead to higher demand for residential development, commercial uses and investor interest in nearby projects.

- Improved transportation network

- Reduced urban congestion

- Better accessibility

- Higher investment appeal

- Increased property demand

Nearby Housing Societies and Landmarks

The DHA Gandhara Islamabad location is near to several prestigious housing societies. These surrounding projects contribute to the value by fostering a bigger urban environment and commercial activities.

Capital Smart City, Blue World City, DHA Phase 6 Islamabad, DHA Phase 7 Islamabad, Faisal Town Phase 2 are some of the most eminent development projects in and around Islamabad. These developments bolster the area’s growth prospects.

- Capital Smart City

- Blue World City

- DHA Phase 6 Islamabad

- DHA Phase 7 Islamabad

- Faisal Town Phase 2

DHA Gandhara Islamabad Master Plan and Location Synergy

The proposed master plan is based on the advantages of the project’s location. The residential areas, commercial centres, health care centres, educational institutions, and recreational facilities are expected to be present in DHA Gandhara.

Projects can be more successful in meeting market needs and add greater value when they are well planned and linked to strategic connectivity. DHA Gandhara is appealing for both present and future residents as well as investors.

- Integrated community design

- Residential districts

- Commercial zones

- Educational facilities

- Recreational amenities

Current 1 Kanal File Rates in DHA Gandhara

Currently, investment activity is focused on Land Provider files as the project is still in the pre-launch phase. These are the files that give the investors a chance to get a head start.

The market price of a 1 Kanal LP file is around PKR 60 lacs today. These rates are expected to rise after the official launch announcements and plot allocations are made

- 1 Kanal LP File

- Approximate Rate: PKR 60 lacs

- Pre-launch opportunity

- Active investor demand

- Potential future appreciation

Membership Charges and Total Investment Cost

Investors have to pay membership fees, tax fees, in addition to the file cost. The current estimates of the above expenses are around PKR 2.70 lacs.

If the file price is added to this, the total amount spent for acquisition is about PKR 62.70 lacs. This is the investment point prior to official launch pricing.

- File Price: PKR 60 lacs

- Membership Charges: PKR 2.70 lacs

- Total Cost: PKR 62.70 lacs

- Development charges separate

- Early-stage pricing advantage

DHA Gandhara Islamabad Payment Plan Expectations

The official DHA Gandhara Islamabad payment plan has yet to be published. Based on market expectations, however, DHA is likely to provide flexible installments after the project officially kicks off.

The development charges of a 1 Kanal plot is likely to be PKR 20 – 25 lacs. Such charges will probably be paid straight to DHA via a controlled payment construction.

- Official plan awaited

- Flexible installments expected

- Development charges separate

- Estimated charges PKR 20–25 lacs

- Investor-friendly structure anticipated

Future Growth Outlook Based on Location

The location advantage is an important element of the growth potential of DHA Gandhara. The airport corridor, Ring Road connectivity, motorway access and surrounding developments provide a good base to appreciate in the long term.

The building up of infrastructure and the rising development projects will lead to a high demand of residential and commercial properties. This situation can be expected to lead to significant gains in value over the next few years.

- Airport corridor expansion

- Ring Road development

- Motorway connectivity

- DHA brand reputation

- Rising property demand

Conclusion

The DHA Gandhara Islamabad location is definitely one of the best assets of the project. The development is close to Rawalpindi Ring Road, Motorway M-2, Chakri Interchange and Islamabad International Airport, ensuring its excellent connectivity and its future growth prospects. The infrastructure benefits are anticipated to provide a boost to the residential demand as well as further commercial development.

The current 1 Kanal LP is sold at the rate of around PKR 60 lacs with membership fee of around PKR 2.70 lacs making the acquisition cost around PKR 62.70 lacs. Potential investors still consider DHA Gandhara Phase 9 Islamabad as a long-term investment opportunity as the official DHA Gandhara Islamabad payment plan is yet to arrive, and the development cost is expected to be between PKR 20 lacs to 25 lacs.

FAQs

What is DHA Gandhara Islamabad?

DHA Gandhara Islamabad is an upcoming DHA housing project planned near Islamabad International Airport.

What is the DHA Gandhara Islamabad location?

The project is expected to be located near Motorway M-2, Chakri Interchange, and Rawalpindi Ring Road.

What is the current 1 Kanal file price?

The current market demand for a 1 Kanal LP file is approximately PKR 60 lacs.

What are membership charges?

Membership and tax charges are estimated at approximately PKR 2.70 lacs.

What is the total acquisition cost?

The estimated acquisition cost is approximately PKR 62.70 lacs excluding development charges.

What are the expected development charges?

Development charges for a 1 Kanal plot are expected to range between PKR 20 and 25 lacs.

Has the DHA Gandhara Islamabad payment plan been announced?

No, the official DHA Gandhara Islamabad payment plan has not yet been released.

Why is the location important for investment?

The location provides access to the airport, motorway, Ring Road, and major housing developments, supporting future growth and appreciation.

Why the Way You Care for Shoes Says More Than the Shoes Themselves

Heavy Equipment Downtimes | Contractor Solutions

Electrician Exams |5 Signs You Are Ready

Recovery Gift Baskets Gift Guide

Office Wiring Systems Power Over Ethernet

Hair thinning solutions 5 easy ways

The 15 Highest-Paid Rugby Players in the World

Christopher Dare: The Untold Story of Engineer and Former Husband of Angela Rippon

How to Ensure Your Home is Valued Correctly for a Quick Sale

Nancy Hallam: The Inspiring Life, Career, and Success Story Behind Ian Wright’s Wife

Who Is Maisie Mae Roffey? The Private Life, Family Story, and Quiet Success of Julie Walters’ Daughter

Simon Dixon Biography: Lifestyle, Net Worth, Family, Career and Success Story

The 15 Highest-Paid Rugby Players in the World

Christopher Dare: The Untold Story of Engineer and Former Husband of Angela Rippon

How to Ensure Your Home is Valued Correctly for a Quick Sale

Nancy Hallam: The Inspiring Life, Career, and Success Story Behind Ian Wright’s Wife

Who Is Maisie Mae Roffey? The Private Life, Family Story, and Quiet Success of Julie Walters’ Daughter

Simon Dixon Biography: Lifestyle, Net Worth, Family, Career and Success Story

-

Sports2 months ago

Sports2 months agoThe 15 Highest-Paid Rugby Players in the World

-

Celebrity8 months ago

Celebrity8 months agoChristopher Dare: The Untold Story of Engineer and Former Husband of Angela Rippon

-

Real Estate6 months ago

Real Estate6 months agoHow to Ensure Your Home is Valued Correctly for a Quick Sale

-

Celebrity8 months ago

Celebrity8 months agoNancy Hallam: The Inspiring Life, Career, and Success Story Behind Ian Wright’s Wife

-

Celebrity8 months ago

Celebrity8 months agoWho Is Maisie Mae Roffey? The Private Life, Family Story, and Quiet Success of Julie Walters’ Daughter

-

Business7 months ago

Business7 months agoSimon Dixon Biography: Lifestyle, Net Worth, Family, Career and Success Story

-

Celebrity9 months ago

Celebrity9 months agoJohnny Carell: Inside the Life, Family, and Rising Success of Steve Carell’s Son

-

Celebrity6 months ago

Celebrity6 months agoDraven Duncan: Tim Duncan’s Rising Star Son and His Inspiring Basketball Journey